Article

A Critical Analysis Of National Anti-Profiteering Authority And Its Constitutional Validity

This article deals with the validity and the constitutionality of Section 171 of CGST and the challenges which are faced by the implementation of this section, due to the uncertainty in the scope of Section 171 writes Harshal Sareen.

-

Harshal Sareen

Harshal Sareen

INTRODUCTION

While implementing the significant and most important tax reform in India, it created a lot of benefits and controversies in the corporate world in India, which has resulted in unfamiliarity with the significant law pertaining to ‘Anti Profiteering Measure’. This concept has been ingrained in Section 171 of CGST (Central Goods and Services Tax Act, 2017), which has proved to be both uncertain and interesting at the same time. After passing the third order National Anti-Profiteering Authority(hereafter “NAA”) it is to be observed how the GST Acts would work upon in the future regarding the ‘socialistic’ aspect. By this it is intended to explain initially the nature and character of t or dangerous provision. NAA has also been significantly affected upon the implementation of Goods and Services Acts. The primary purpose of the provision is to mitigate and circumscribe the increase in inflation owing to implementation of the humungous reform in the field of tax.

Through several experience and shedding the light upon how the provision can be proved to be a toothless from many countries it can be inferred and experienced that implementation of any reform in the tax system a transient period of inflation follows. Therefore, the law-makers learning from the several incidents have decided to provide for a provision to protect in the act itself. 1 Many countries like Malaysia and Australia have adopted identical measures to prevent the inflation after such reform in tax system. 2 Taking into account recent reports, it can be clearly observed that the result of such a significant reform in the tax system hasn’t shown any signs of inflation. 3

2. Part VIII A, The Competition and Consumer Act, 2010 (Australia); The Price Control and Anti Profiteering Act, (2011) (Malaysia).

3. Atul Gupta, Why was there no inflationary impact of GST?, Financial Express (07/06/2018) available at: https://www.financialexpress.com/opinion/why-was-there-no-inflationary-impact-of-gst/1196472/, last seen 01/06/2020.

Despite such conditions, the section bestow that the supplier has to shrink the price of a good in a proportionate manner, in the following conditions when: (i) a benefit of tax has accrued to the supplier, (ii). A reduction in the rate of tax on any supply of goods. 4 It can be easily understood though an example, if the price of any particular good is ₹. 1000 and tax imposed on such good is ₹. 200 and the good were further sold for ₹. 1200, then after the reform in the tax system, the new tax imposed was reduced to ₹. 180, then such good shall be sold for ₹1180 rather than ₹1200.

The aforesaid provision can be considered to be violative of Article 14 and Article 19 of the Indian Constitution. Since the principle of equality has been breached with the uncontrolled choice of the executive and unguided discretion, which is arbitrary in nature. No precise definition of ‘commensurate reduction’ has been provided in the act hence, no guideline has to be followed. Drafting a policy is the most pivotal function of legislature which cannot be delegated, but in this case, giving such unconstraint powers amounts to excessive delegation. The Preamble of the act is also silent as to the definiteness of the power. Article 19 (1) (g) is being violated because the inherent profit motive of the traders is undermined. The reasonable restrictions for interests of the general public are also not visible.

The CGST Rules framed there under are also unconstitutional in nature, since the subordinate legislation is manifestly arbitrary. No care and deliberation is found. Hence, Article 14 is violated. Also, the price reduction is being forced upon the traders which violate Article 19 (1) (g). Even the test of proportionality that has been evolved by the courts for imposing reasonable restrictions is being not fulfilled. The sufficiency in terms of importance is also not deductible.

PREVIOUS TAXES, CESS AND ANTI -PROFITEERING

The foremost condition which has been provided under this section is that any decrease in the tax levied on the commodity shall be carry forward to the buyer of such good in such a manner that price of the commodity shall be reduced commensurately. Therefore, it is necessary and significant to understand the ambit and the meaning of the term ‘tax’, which has not been defined explicitly in the Act, therefore it has to interpreted through the general interpretation that the term tax shall include all the tax which are levied on a particular service/good. As a consequence, sum of all the tax levied on the commodity before the GST regime shall be compared to the present rate of GST.

But a question arises that whether the ‘cess’ would be considered under the ambit of the word ‘previous tax’ or not, as the act is silent about this for the purpose of anti-profiteering. NAA in its two out of three orders of have included cess for the purpose of pre-GST tax. 5 The procedures have been adopted by NAA arbitrarily. The legislature has inquired the NAA to decide the procedure to find out whether any ‘commensurate reduction of price’ has been there or not. 6 The minor tax applied in the form of cess can be of a great importance in the tax incidences.

CONSTITUTIONAL VALIDITY OF ANTI PROFITEERING

A. SECTION 171 OF CGST ACT IS UNCONSTITUTIONAL SINCE IT VIOLATES ARTICLE 14 OF THE CONSTITUTION.

Under the Central Goods Services Tax Act, 2017, 7 the anti-profiteering provisions are introduced to ensure that the reduction in the tax incidence is passed on the customer and not retained by the supplier. Section 171 of the said act provides for the ‘Anti- Profiteering Measure’, wherein the rationale as provided in the online government pamphlet 8 is based on the ‘experience of many countries’ where marked increase in the prices has been observed by the government on the introduction of Goods and Services Tax respectively. 9 But the implementation of such provision in India violates the constitutional rights guaranteed in the Constitution, since it amounts to vesting of unguided discretion in the executive authorities and an arbitrary action on part of the state. Furthermore, the said section can be said to be violative of Section 171 as it provides unguided discretion being vested in the executive authorities. Discretion has been defined as “a science or understanding to discern between falsity and truth, between right and wrong and not to do according to will and private affection.” 10

6. G. Khattar and N. Mendiratta, GST and Anti-Profiteering Law! Are we complying? Is the Government ready?, Gst Connect (06/11/2017) available at: http://blog.simbizz.in/2017/11/gst-and-anti-profiteering-law-are-we.html, last seen 30/05/2020.

7. Supra 4.

8. A. Reddy, Legality of GST’s Anti- Profiteering Provision, Live Mint (27/02/2018) available at:

https://www.livemint.com/Opinion/IbZ1gNXgywVhtqpSvNGRzK/Legality-of-GSTs-antiprofiteering-provision.html, last seen 04/06/2020.

9. National Anti- Profiteering Authority, available at: http://www.naa.gov.in/page.php?id=about-naa, last seen 08/06/2020.

10. I.P. Massey, Administrative Law, 98 (Eastern Book Company, 7th ed., 2015).

When the scope of discretion is provided, it can only be exercised fairly and reasonably; otherwise, the act is void on the ground that there was no valid exercise of discretion in the eye of law. 11 Unguided discretion and uncontrolled choice of the executive is contrary to the mandate of equality being provided in the Constitution which can be inferred from the judgment of Suman Gupta v. State of Jammu & Kashmir. 12 Such discretion is arbitrary because it is capable of being used arbitrarily to favor one party over the other. 13 The absence of arbitrary power is the first postulate of rule of law upon which our entire constitutional edifice is based. 14 Constitutional principle of equality is inherent in rule of law. 15

Section 171 (1) of the said Act mentions “commensurate reduction in prices”, which has been held mandatory on part of the supplier. 16 The authority so constituted under the sub- section 2 of the same provision is being provided with such powers and functions which are not circumscribed in the act. 17 No guideline or criteria is being provided in the act by the legislature so as to determine what is ‘commensurate’, because the Central Goods and Services Tax (CGST) Rules, 18 Rule 126 governs this aspect of ‘commensurate’ reduction. The Methodology and procedure is left at the hands of the Authority so constituted. This shows unlimited discretion being vested in an executive authority through the legislative provision that gives vague and uncertain terminologies. Equality before law and absolute discretion to grant or deny benefit of the law are diametrically opposed to each other and cannot coexist. 19Hence, equality before law is negated with the said provision and same must be held as unconstitutional.

12. Suman Gupta v. State of Jammu and Kashmir, (1983) 4 SCC 339.

13. Rajwanshi v. State of U.P., AIR 1988 SC 1089.

14. DD Basu, Constitution of India, 1473(Lexis Nexis, 2014).

15. Ibid. at 1475.

16. Supra, 4.

17. Ibid.

18. Central Board of Indirect Taxes and Customs, available at:

http://www.cbic.gov.in/resources//htdocs-cbec/gst/CGST-Rules-2017-Part-A-Rules.pdf;jsessionid=7D872D5B9BACF0A87D798F2E3D2A1349, last seen 03/11/2019.

19. Sudhir Chandra v. Tata Iron & Steel Co. Ltd., AIR 1984 SC 1064.

B. SECTION 171 OF THE CGST ACT IS UNCONSTITUTIONAL BEING VIOLATIVE OF ARTICLE 19 (1) (G).

Under Article 19(1) (g) of the Constitution, a citizen has the right to practice any profession, or to carry on any occupation, trade or business. 20 It is been held that a company is not a citizen, hence it cannot maintain a petition for enforcement of fundamental right under Article 19, 21 though a shareholder is given the right to invoke the fundamental rights if the same are violated. 22 Hence, though a company being a non- citizen cannot have any fundamental right under Article 19 (1), but it can contend that the impugned provisions infringe the fundamental rights of a citizen and hence void. 23

To infer from a course of transactions that it is intended thereby to carry on business, ordinarily there must exist the characteristics of volume, frequency, continuity and system indicating an intention to continue the activity of carrying on the transactions for a profit. 24 Production, distribution and consumption of wealth are integral part of the terminology. 25 But in the word “trade”, an explicit profit motive is found to be essential by the courts, whereby in its nature of business, being manual or mercantile, runs through an inherent profit motive. 26 Both these terminologies have also been used simultaneously by the courts to mean some real substantial and systematic or organized course of activity or conduct with a set purpose. 27

But when the price is fixed, regulated or controlled by the government, it essentially acts as a clog on this right to trade. 28 Prices are generally to be governed and regulated by the market forces. 29

21. State Trading Corporation of India Ltd. v. Commercial Tax Officer, Vishakhapatanam, AIR 1963 SC 1811.

22. Bennett Coleman & Co. & Ors v. Union Of India, AIR 1972 SC 106; see also Mahindra & Mahindra Ltd., Bombay v. State of Andhra Pradesh, AIR 1986 AP 332.

23. Arvind Mills Ltd., Ahmedabad v. State Of Gujarat, ILR (1966) Guj. 313.

24. Director of Supplies & Disposals v. Board of Revenue, AIR 1967 SC 1826.

25. Safdarjung Hospital v. Kuldip Singh Sethi, (1970) 1 SCC 735.

26. State of Punjab v. Bajaj Electricals Ltd., AIR 1968 SC 739.

27. State of Bihar v. Harihar Prasad Debuka, (1989) 2 SCC 192.

28. Indraprastha Gas Ltd. v. Petroleum and Natural Gas Regulatory Board and Anr., 2012 SCC Online Del 3215.

29. Ibid.

It has been categorically held that a power of imposing restrictions on profit percentages does not encompass within itself the right to exercise power in manner that inhibits terms of contract and freedom granted therein. 30 Essentially, price fixation is a legislative function. 31

Thus, the power so provided to the NAA so created under Sub Section 2 of Section 171 of the CGST Act leads to a clog on business entities to decide the prices as per the reduction in the tax rate by the Government. The freedom to pursue the profit motive is taken away from the businesses and trade is being regulated with no justification in the reasonable restrictions. 32 It is because the interpretation for the reasonability for restrictions that can be imposed upon this fundamental right, as laid down by the Supreme Court is not fulfilled.

C. THE COMPOSITION OF THE NAA AS PRESCRIBED UNDER THE CGST RULES, 2017 IS ILLEGAL AND UNCONSTITUTIONAL.

The composition of the NAA as prescribed under the Central Goods and Services Act 33 is illegal and unconstitutional. NAA is a statutory body constituted under section 171 of CGST Act to examine whether input tax credits availed by any registered person or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods or services or both supplied by him. Further, the composition of the body as per NAA includes the following members. The Authority shall consist of,-

- (a) a Chairman who holds or has held a post equivalent in rank to a Secretary to the Government of India; and

- (b) Four Technical Members who are or have been Commissioners of State tax or central tax for at least one year or have held an equivalent post under the existing law, to be nominated by the Council. 34

The provisions of CGST Act and CGST Rules related to composition of NAA are unconstitutional and illegal. These provisions strike at the root of the Independence of Judiciary and Doctrine of Separation of Powers. NAA is a quasi-judicial authority and being a quasi-judicial authority its competition has to comply with certain principles laid down by the Supreme Court and the instant fails to abide by them.

31. Transmission Corporation of Andhra Pradesh Limited v. Sai Renewable Power (P) Ltd. (2011) 11 SCC 34.

32. Art. 19, the Constitution of India.

33. Supra 4.

34. Central Goods and Services Tax Rules, 2017, I CBEC 122 (India).

A. A. THE NATIONAL ANTI-PROFITEERING AUTHORITY IS A QUASI JUDICIAL AUTHORITY.

NAA is a quasi-judicial authority. All the characteristics of a quasi-judicial authority are squarely covered by NAA. In the judgment of State of Gujarat v. Gujarat Revenue Tribunal Association the Apex Court of India observed that an authority is a quasi-judicial body if:

- • the statutory authority is empowered under a statute to do any act,

- • the order of such authority would adversely affect the subject and,

- • Even though there is no list or two contending parties, and the contest is between the authority and the subject, and

- • the statutory authority is required to act judicially under the statute, the decision of the said authority is a quasi-judicial decision. 35

NAA is also a quasi-judicial authority as it qualifies for all the features mentioned in the above-mentioned judgment. NAA is a statutory body whose order affects the parties and it is entrusted to handle the matters judicially. Infact, as per Rule 132 of CGST Rules 36 NAA is empowered to summon persons to give evidence and to produce documents. Powers of Court are entrusted with NAA to take evidence and provisions of CPC are also made applicable, which clearly indicate towards the fact that NAA is performing judicial functions. As per the report of Law Commission of India 37, “An authority is quasi-judicial in nature if it is created under a statute and it is empowered to take a decision which affects the rights of persons and such an authority under the relevant law required to make an enquiry and hear the parties, decision rendered by it is a quasi-judicial act”. All the characteristics mentioned by the Law Commission are also covered well by the NAA, which again draws the same conclusion that NAA is a quasi judicial authority.

FIGHTING ANTI PROFITEERING

The litigation process for fighting up the anti-profiteering is quite burdensome and substantial. The parties or persons which can file a suit for anti-profiteering are explicitly provided under the act itself.

36. Central Goods and Services Tax Rules, 2017, I CBEC 122 (India).

37. 272nd Law Commission of India Report, Assessment of Statutory Framework of Tribunals in India, 50 (2017), available at:

http://lawcommissionofindia.nic.in/reports/Report272.pdf.

The scope of filing a suit against any institution has been broadened up by providing the clause of ‘any other person’. 38 It may even lead to exploitation of the MNC’s because the suit can be filed by any person and against any person, even against the competitor from the industry of the similar product.

The ‘issues pertaining to local nature’ again creates the ambiguity in determining that what shall be considered within the ambit of local nature. Therefore, it has to be determined though the interpretation. It can be interpreted that the services and the goods concerning to a specific and particular area would be considered under the term local nature.

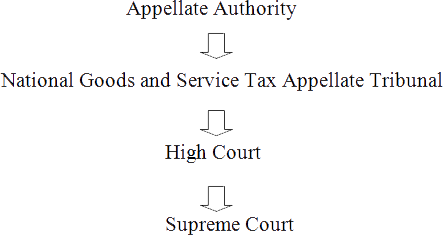

Initially the application is adjudicated by these institutions or authorities. Firstly, through State Level Screening Committee (Issues of Local Nature), then secondly the application is forwarded and scrutinized through Standing Committee, thirdly, through Director General Of Safeguards and finally through National Anti-Profiteering Authority. Furthermore, it can be followed by-

Judicial process can go through the endless eight-levels; such a process would create the hardship for the MNC’s.

NAA - A TOOTHLESS PROVISION

The provisions by the NAA can sometimes to be proved to be a toothless provision, or in other words the anti-profiteering measures can be proved completely useless. Essentially it may be due to the fact because of the difficulty to implement such provision and lack of guidelines. 39 And another significant reason which can prove this provision to be completely redundant is that the manufacturers and the suppliers of the commodities may have increased the price of the commodity before the roll-out of GST and then may further decrease the prices of the commodity. Such a scenario violates and derogates the primary purpose of the formation of such law or provisions. And as stated above such section also violates the fundamental rights conferred under Article 14 and 19 of the Indian Constitution, which again makes section 171 of the Act a toothless provision.

39. R. Singhal, Anti-Profiteering- A Concept in GST Law, Taxmann.com, 91, 401 (2018).

CONCLUSION

It has been suggested by many authors, that the CCI shall also be for formation and development of procedures as this institution has experience in this particular field of unfair practices by the manufacturers. Thus can assist NAA to develop the laws pertaining to anti-profiteering. At the present moment, the law in India doesn’t lay any procedure in order to determine whether any anti-profiteering has occurred or not. However the power for the same has been provided to NAA but due to the lack of proper guidance such power has become completely redundant. Presently, India is using a method similar to Australia (Net Dollar Margin Rule) to determine the amount of anti-profiteering. 40 However, this has not been used rigidly, the ambiguity still prevails. The provisions pertaining to anti-profiteering are uncertain and ambiguous and lack the proper implantation owing to such ambiguities in the act. Furthermore, vesting of unguided discretion in the executive authorities and an arbitrary action on part of the state violates the fundamental right under Article 14 of the Indian Constitution. And it has been well established by the judiciary that unguided discretion and uncontrolled choice of the executive is contrary to the mandate of equality being provided in the Constitution. 41 Moreover, this section also violates Article 19 of the Indian Constitution Conclusively, it can be said that the aforesaid provision can be considered to be violative of article 14 and article 19 of the Indian Constitution as it breaches the principle of equality with the uncontrolled choice of executive and unguided discretion, which is arbitrary in nature. Therefore, such ambiguity in the anti-profiteering law can be proved to be a dangerous weapon or a toothless provision.

Moreover in order to create deterrence in the market and prevent anti-profiteering which the primary purpose of the section and the institution of NAA itself, the name should be disclosed by the NAA who is involved in anti-profiteering. As in one of the case of HUL wherein it was accused for not providing the benefits in several segments, so in order to safeguard its reputation it decided to distribute the profit which was created illegally, however it was rejected by the government, which reflects that such a measure create a deterrence of harming the reputation. 42

https://thewire.in/business/gsts-anti-profiteering-provisions-lndian-socialism, last seen 20/05/2020.

41. Supra, 13.

42. N. Agnihotri, Anti-Profiteering under GST: Provisions, Validity, Issues & Challenges, 93 Taxmann.com, (2018).

- FIR Copy of Mahatma Gandhi assasination case

- Licito Concurso'20

- Rules for Licito Concurso '20- A National Legislative Drafting Competition

- Registration Form for Licito Concurso-20

- www.apexcourtweekly.substack.com

- www.lawupdater.com/wp/

- XIIIth K.K. Luthra Memorial Moot Court Competition 2017

- President of India Presented with the First Copy of the Book Statement of Indian Law Published by Thomson Reuters